#autocorrelation

Autocorrelation

Correlation of a signal with a time-shifted copy of itself, as a function of shift

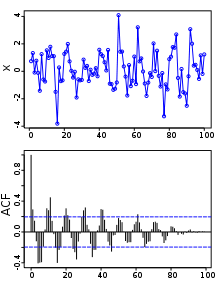

Autocorrelation, sometimes known as serial correlation in the discrete time case, is the correlation of a signal with a delayed copy of itself as a function of delay. Informally, it is the similarity between observations of a random variable as a function of the time lag between them. The analysis of autocorrelation is a mathematical tool for finding repeating patterns, such as the presence of a periodic signal obscured by noise, or identifying the missing fundamental frequency in a signal implied by its harmonic frequencies. It is often used in signal processing for analyzing functions or series of values, such as time domain signals.

Tue 17th

Provided by Wikipedia

This keyword could refer to multiple things. Here are some suggestions: