#wiener_process

Wiener process

Stochastic process generalizing Brownian motion

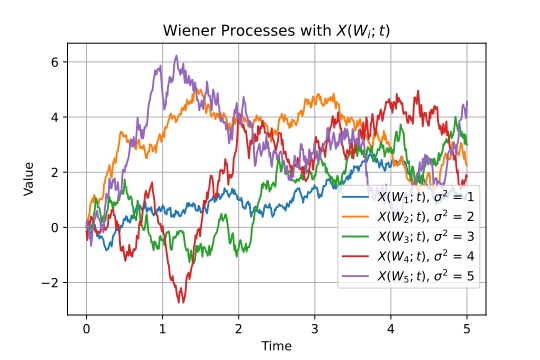

In mathematics, the Wiener process is a real-valued continuous-time stochastic process named in honor of American mathematician Norbert Wiener for his investigations on the mathematical properties of the one-dimensional Brownian motion. It is often also called Brownian motion due to its historical connection with the physical process of the same name originally observed by Scottish botanist Robert Brown. It is one of the best known Lévy processes and occurs frequently in pure and applied mathematics, economics, quantitative finance, evolutionary biology, and physics.

Tue 30th

Provided by Wikipedia

This keyword could refer to multiple things. Here are some suggestions:

0 searches

This keyword has never been searched before

This keyword has never been searched for with any other keyword.